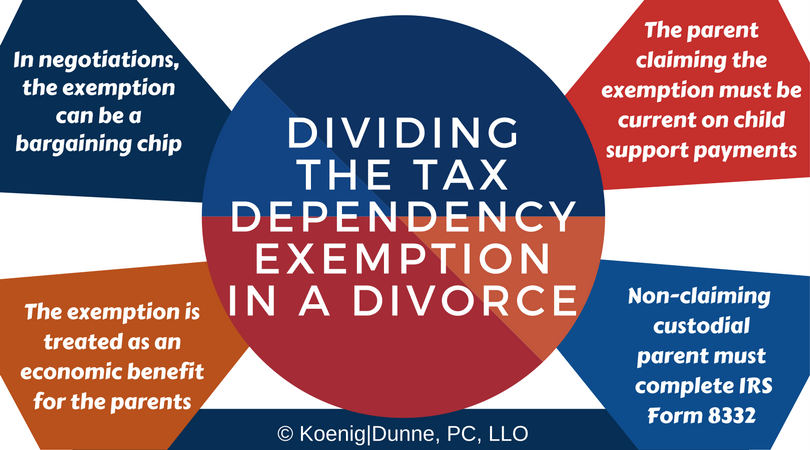

The federal government allows taxpayers to exclude from their income an exemption amount for each person who is a dependent of the taxpayer for that taxable year. You can claim a tax dependency exemption if you are a parent who provides support to a dependent minor child. But what happens after divorce when you no longer file joint returns? In Nebraska, the tax dependency exemption is considered an economic benefit similar to an award of child support or alimony. If the parents do not agree how the exemption should be allocated, the judge hearing the divorce case has the power to determine which parent gets to claim the exemption. It may be fair to award the exemption to one parent every year, it may be inequitable to allow a parent to claim the exemption, or it may be fair to award the exemption to both parents on an alternating basis. How will a court decide?

Generally, the custodial parent is entitled to claim the dependency exemption because he or she has the child in his or her care for a majority of the taxable year. It is presumed that a parent with sole physical custody is likely to incur more expenses for the child, so allowing the custodial parent to claim the exemption is fair. However, this is a presumption that may be rebutted. If the non-custodial parent wishes to claim the exemption, whether every year or alternating years, he or she will have to show that he or she provides financial support to the child and should be entitled to claim the economic benefit.

If you are the non-custodial parent, you may be entitled to share in claiming the tax dependency exemption if you:

- Pay child support;

- Contribute to your child’s work or education-related day care expenses; or

- Contribute to your child’s medical expenses.

However, courts have held that a parent who pays a “relatively small amount” of child support may not be entitled to share or claim the exemption. The primary purpose in reallocating the exemption is to allow the parent financially supporting the child to have more disposable income from which to make such a payment. If a parent’s child support obligation is relatively small, then the parent who pays the majority of the child’s expenses should get to claim the exemption.

If there is more than one child for whom the exemption may be claimed, you can get creative on how the exemptions should be allocated. Here are some common ways the exemption(s) is allocated between parents:

- If there is one child –

- One parent gets to claim the exemption every year, or

- The parents alternate the exemption, with one parent claiming in even-numbered years and the other claiming in odd-numbered years.

- If there are two children –

- One parent gets to claim both, or

- Each parent gets to claim one and when there is only one child for whom the exemption applies (e.g., the older child turns 19), the parents alternate the exemption.

- If there are three children –

- Each parent gets to claim one, then the third exemption alternates, or

- One parent gets to claim two, the other claims one, or

- One parent claims all three.

Some helpful notes:

- If your decree does not specify who gets to claim the exemption, the federal government will presume the custodial parent should claim it.

- In Nebraska, a parent is only entitled to claim the exemption if he or she is current in his or her child support obligations.

- If you are the custodial parent and you are releasing your right to claim the exemption (whether it’s because your decree orders you to or otherwise), you will need to execute IRS Form 8332, found here, in order to formally release your claim to the exemption.

When choosing your divorce attorney, look for one with the knowledge of how the courts and the tax code impact your financial future.

Lindsay Belmont